What is the Soil Stabilization Market Overview – Definition, scope, and significance?

Soil stabilization refers to the process of improving the engineering properties of soil to increase its load‑bearing capacity, reduce permeability, and enhance durability. The market encompasses a wide range of technologies, including mechanical compaction, chemical admixtures, polymeric binders, and mineral additives, applied across sectors such as construction, transportation, agriculture, and industrial infrastructure. Its significance lies in enabling cost‑effective road construction, extending the service life of pavements, mitigating settlement issues, and supporting sustainable land development by reducing the need for new raw materials.

What are the Soil Stabilization Market Drivers, Restraints, Challenges, and Opportunities?

Key drivers include rapid urbanization, increasing demand for durable road networks, and stricter environmental regulations that favor low‑emission construction practices. The growing awareness of soil erosion and the need for agricultural land productivity also propel market growth. Restraints stem from high initial costs of advanced chemical stabilizers and limited skilled labor for specialized mechanical techniques. Challenges involve regulatory approvals for new additives and the variability of soil types across regions. Opportunities arise from innovations in polymer‑based stabilizers, the integration of renewable bio‑additives, and government incentives for infrastructure repair projects.

What are the current Soil Stabilization Market Growth Trends?

Emerging trends include the adoption of hybrid stabilization methods that combine mechanical compaction with chemical or polymer additives to achieve superior performance. The market is witnessing a shift toward eco‑friendly polymers derived from waste plastics and bio‑based resins, aligning with sustainability goals. Digital monitoring tools, such as real‑time moisture sensors and AI‑driven compaction analytics, are enhancing construction precision. Additionally, increasing use of recycled construction and demolition waste as a stabilizing aggregate is gaining traction in developed economies.

How has COVID‑19 impacted the Soil Stabilization Market and what is the recovery trajectory?

The pandemic caused temporary project delays and supply‑chain disruptions for raw materials, leading to a short‑term dip in demand. However, stimulus packages focused on infrastructure revitalization accelerated post‑pandemic recovery. Governments prioritized road repair and rural connectivity, boosting demand for rapid‑cure stabilization solutions. The market has rebounded strongly and is projected to continue this upward momentum, supported by renewed construction activity and increased public‑private partnership investments.

What does the Soil Stabilization Market Competitive Landscape look like?

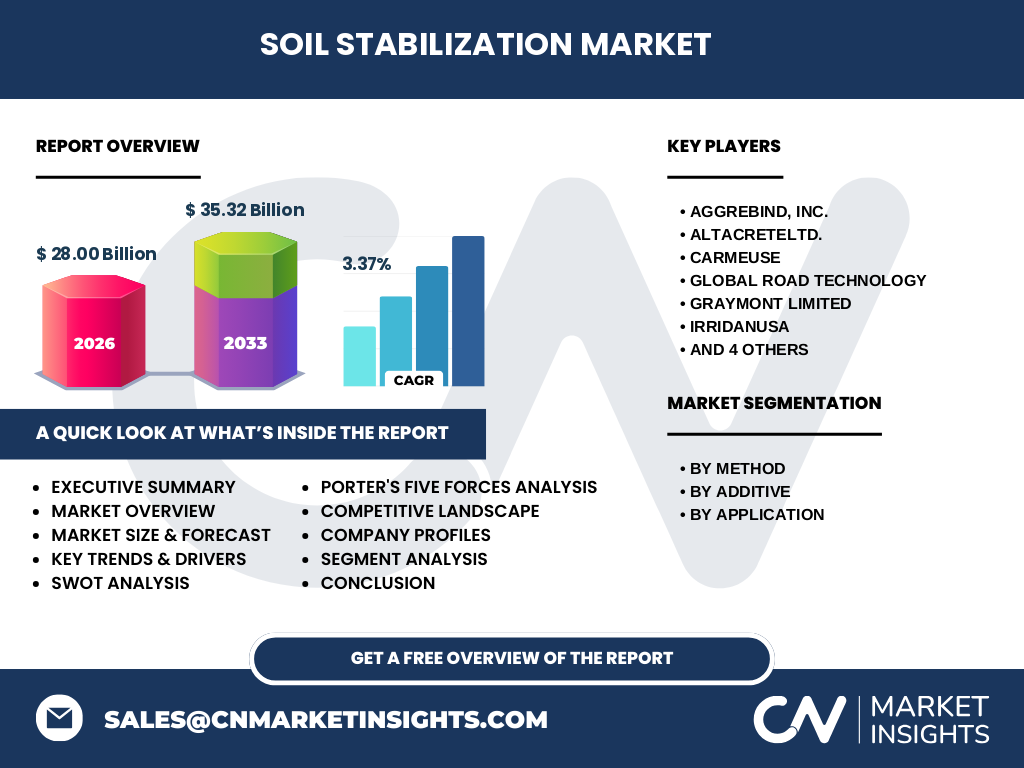

The competitive environment is characterized by a mix of global conglomerates and specialist firms. Major players such as Aggrebind, Inc., AltaCrete Ltd., Carmeuse, Global Road Technology, Graymont Limited, Irridan USA, SNF Holding, Soilworks LLC, Tensar International Limited, and Wirtgen Group dominate through extensive product portfolios, strategic acquisitions, and geographic expansion. Market consolidation is evident with several recent mergers aimed at broadening additive offerings and strengthening service networks.

Can you provide an Executive Summary of the Soil Stabilization Market?

The Soil Stabilization Market is valued at $28.00 billion in 2026 and is expected to reach $35.32 billion by 2033, reflecting a CAGR of 3.37 % over the forecast period. Growth is driven by infrastructure expansion, sustainability imperatives, and technological innovations in polymer and mineral additives. The market is segmented by method (mechanical, chemical), by additive (polymers, minerals and stabilizing agents), and by application (industrial, non‑agricultural, agricultural). North America and Europe hold the largest shares, while Asia‑Pacific exhibits the fastest growth owing to massive road‑building programs. Leading companies are focusing on product differentiation and strategic partnerships to capture emerging opportunities.

What are the Soil Stabilization Market Forecasts for 2025‑2032?

Based on the provided CAGR of 3.37 %, the market is projected to expand from its 2026 baseline of $28.00 billion to approximately $35.32 billion by 2033. This steady growth reflects continuous infrastructure investments, rising adoption of advanced stabilizers, and expanding applications in agricultural land management. The forecast underscores a consistent upward trajectory without major volatility, indicating a stable investment climate.

How is the Soil Stabilization Market sized and shared by segmentation?

The market is divided into three primary dimensions. By method, mechanical stabilization accounts for traditional compaction techniques, while chemical stabilization covers additives such as cementitious and polymeric binders. By additive, polymers are gaining market share due to their flexibility and environmental benefits, whereas minerals and stabilizing agents (e.g., lime, fly ash) remain essential for cost‑sensitive projects. By application, the industrial segment includes airports, ports, and heavy‑duty pavements; non‑agricultural covers highways, urban roads, and municipal projects; agricultural focuses on field leveling, irrigation channels, and erosion control. Each segment contributes uniquely to the overall market, with chemical and polymer‑based solutions experiencing the strongest growth rates.

What is the Global Soil Stabilization Market size and share by region?

Geographically, North America and Europe collectively represent the largest portions of the global market, driven by mature infrastructure networks and stringent environmental standards. The Asia‑Pacific region is the fastest‑growing market, fueled by extensive highway construction, rapid urbanization, and government‑backed infrastructure programs. The Middle East & Africa and Latin America show moderate growth, primarily in urban development and agricultural enhancement projects.

What does the Regional Analysis of the Soil Stabilization Market reveal?

In North America, demand is propelled by aging highway systems and significant federal funding for road rehabilitation, with a strong preference for low‑emission polymer additives. Europe’s market is shaped by circular‑economy policies encouraging the use of recycled aggregates and mineral stabilizers. Asia‑Pacific’s expansion is driven by massive projects in China, India, and Southeast Asian nations, where cost‑effective mineral additives are common, but there is rising interest in polymer technologies. The Middle East focuses on desert‑soil stabilization for high‑temperature environments, while Latin America emphasizes agricultural land improvement.

Who are the leading companies in the Soil Stabilization Market and what are their strategies?

Key players include Aggrebind, Inc., which emphasizes innovative polymer blends; AltaCrete Ltd., known for rapid‑cure cementitious systems; Carmeuse, a major supplier of limestone‑based additives; Global Road Technology, focusing on integrated mechanical‑chemical solutions; Graymont Limited, offering limestone and limestone‑derived products; Irridan USA, specializing in geopolymer technologies; SNF Holding, a provider of mineral stabilizers; Soilworks LLC, delivering tailored soil‑treatment programs; Tensar International Limited, strong in geosynthetic reinforcement; and Wirtgen Group, integrating stabilization with advanced paving equipment. Their strategies revolve around R&D investment, acquisitions to broaden additive portfolios, and expanding service networks to capture regional demand.

What does Porter’s Five Forces Analysis indicate for the Soil Stabilization Market?

• Threat of new entrants – Moderate: High capital requirements and technical expertise create barriers, but niche polymer innovators can enter. • Bargaining power of suppliers – Low to moderate: Raw material suppliers (lime, cement, polymers) are numerous, reducing supplier leverage. • Bargaining power of buyers – Moderate: Large construction firms and government agencies can negotiate pricing, yet product differentiation limits switching. • Threat of substitutes – Low: Few alternatives to soil stabilization exist for load‑bearing applications. • Rivalry among existing competitors – High: Companies compete on performance, environmental compliance, and cost, driving continuous innovation.

What are the SWOT insights for the Soil Stabilization Market?

Strengths: Proven technology base, essential role in infrastructure longevity, and growing sustainability focus. Weaknesses: High upfront costs for advanced chemicals, dependence on commodity price fluctuations. Opportunities: Development of bio‑based polymers, digital compaction monitoring, and expansion into emerging economies. Threats: Regulatory delays for new additives, volatile construction cycles, and competition from alternative ground improvement methods such as geotechnical grouting.

How does the Soil Stabilization Market value chain operate?

The value chain begins with raw‑material extraction (limestone, fly ash, polymer resins), followed by additive formulation and blending. Next, manufacturers produce packaged stabilizers and mechanical equipment. Distribution channels include specialized distributors, direct sales to contractors, and online platforms. End users—construction firms, municipalities, and agricultural enterprises—apply the products using on‑site mixing or equipment. After‑sales services, such as technical support and performance monitoring, close the loop, reinforcing brand loyalty and encouraging repeat purchases.

What key investment insights can be drawn for the Soil Stabilization Market?

Investors should target companies with strong R&D pipelines in polymer and geopolymer technologies, as these segments promise higher margins and regulatory advantage. Partnerships with equipment manufacturers enhance market reach. Geographic diversification, especially into fast‑growing Asia‑Pacific markets, can offset slower demand in mature regions. Acquisitions of niche additive producers provide rapid entry into emerging product categories. Monitoring government infrastructure spending will help identify short‑term growth catalysts.

What is the conclusion of the Soil Stabilization Market analysis?

The Soil Stabilization Market is on a steady growth path, underpinned by infrastructure renewal, sustainability mandates, and technological progress. With a projected size of $35.32 billion by 2033 and a healthy CAGR of 3.37 %, the sector offers attractive opportunities for manufacturers, service providers, and investors. Companies that innovate in eco‑friendly additives and integrate digital construction tools are poised to capture the largest share of future demand.

What research methodology was employed for this report?

The study combined primary interviews with industry experts, senior managers, and technical specialists, alongside secondary data collection from company filings, market databases, and government publications. Quantitative data were validated through cross‑checking multiple sources, and qualitative insights were synthesized to develop forecasts using the stated CAGR. Scenario analysis considered macro‑economic trends, regulatory developments, and technology adoption rates.

What is the scope of the research?

The research covers global soil stabilization solutions, segmented by method, additive type, and end‑use application. It includes an assessment of major regions—North America, Europe, Asia‑Pacific, Middle East & Africa, and Latin America—focusing on market size, growth drivers, and competitive dynamics. The scope excludes unrelated ground improvement technologies such as deep mixing piles and soil nailing.

Which key companies and recent developments are highlighted in the Soil Stabilization Market?

Key players include Aggrebind, Inc., AltaCrete Ltd., Carmeuse, Global Road Technology, Graymont Limited, Irridan USA, SNF Holding, Soilworks LLC, Tensar International Limited, and Wirtgen Group. Recent developments feature Aggrebind’s launch of a high‑performance polymer stabilizer for rapid road repair, AltaCrete’s acquisition of a regional cement additive manufacturer, Carmeuse’s expansion of limestone production capacity in North Africa, and Wirtgen Group’s integration of stabilization modules into its paving machines. These activities reflect a focus on product innovation, capacity scaling, and strategic alignment with infrastructure initiatives.